Types of Alternative Investment Funds (AIF) in India

Why The Category You Choose Is The Most Important Decision SEBI splits every AIF into one of three categories at the point of registration, and that single choice determines your tax treatment, leverage limits, investor base and regulatory obligations for the life of the fund. Getting this decision wrong is expensive to reverse. […]

Read More

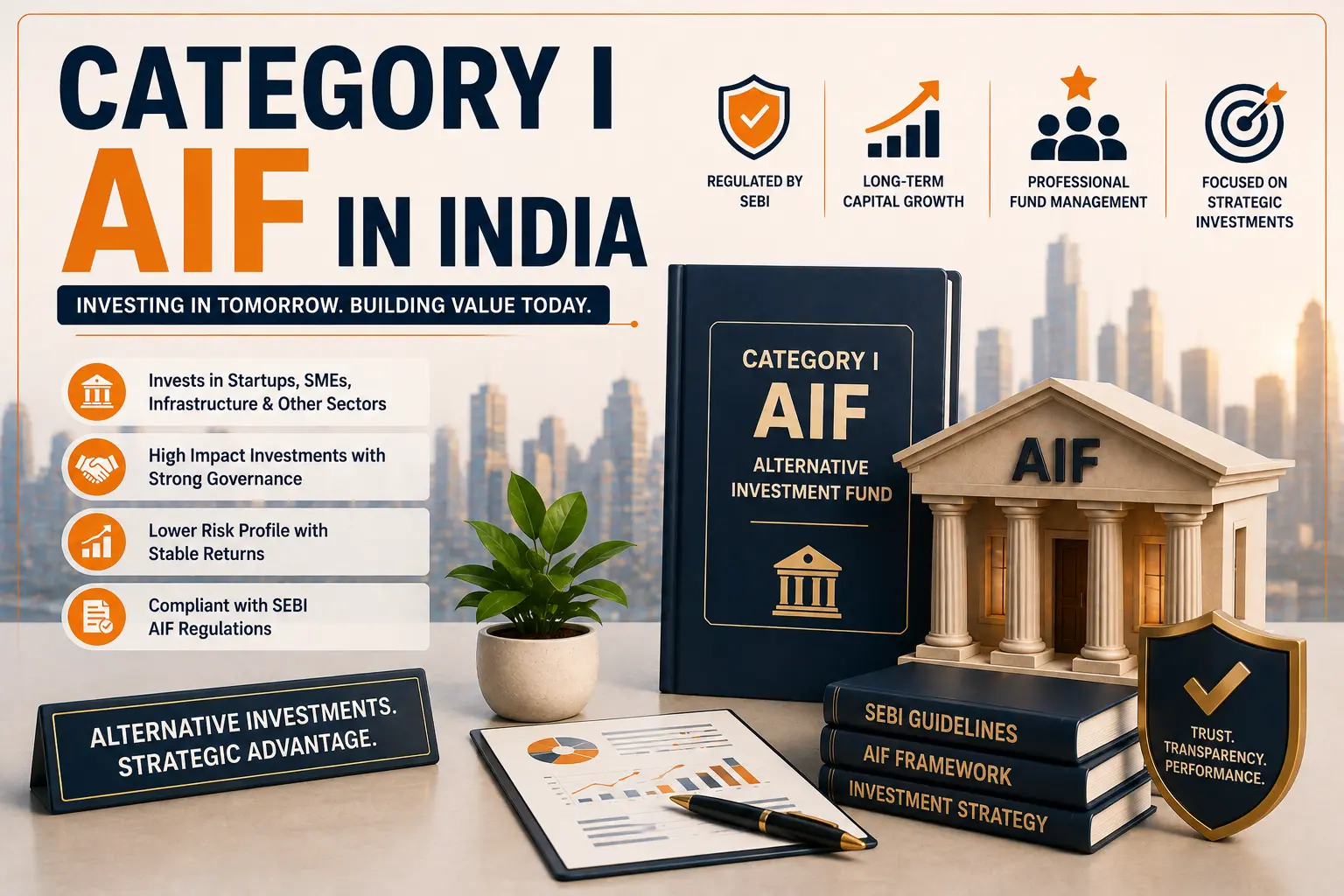

Category I AIF in India

Category I AIFs Why Category I Exists SEBI created Category I specifically for funds that support economically and socially desirable activity: early-stage businesses, MSMEs, infrastructure and social ventures. In exchange, these funds receive a lighter regulatory touch than Category II or III. The Sub-Types Inside Category I Venture Capital Funds: invest in early and growth-stage […]

Read More

How to Start an NBFC in India: Passing the RBI’s “Fit & Proper” and Operational Scrutiny

How to Start an NBFC in India Having ₹10 Crore in the bank is no longer enough to start an NBFC. The Reserve Bank of India (RBI) actively rejects applications that lack a solid operational foundation or experienced management. Starting a Non-Banking Financial Company is less about simply filing paperwork and much more about proving […]

Read More

NBFC vs Nidhi Company vs Microfinance: Which is the Best Structure for Your Lending Business?

Starting a lending or financial services business in India is highly lucrative, but choosing the wrong corporate structure can lead to severe regulatory penalties or stalling due to capital requirements. Entrepreneurs often find themselves confused by the overlapping terminologies and varying compliance demands of different financial entities. The choice ultimately comes down to […]

Read More

NBFC Outsourcing of Financial Services 2026: The April Deadline Is Here and Every Vendor Contract Needs a Review

Outsourcing is how modern NBFCs stay lean. Customer acquisition through fintech partners, credit assessment through analytics platforms, loan servicing through technology vendors, collections through recovery agents, security monitoring through external SOC teams. The operational model depends on third parties at almost every step. And for most of that time, the regulatory framework governing […]

Read More