The single most consequential change to NBFC financial reporting in the last five years completed its final phase on 31 March 2026. The 90-day Non-Performing Asset recognition norm, which the RBI introduced through a phased glide path starting in 2022, is now fully applicable to every NBFC in India without exception. There is no extension. There is no transition relief remaining.

NBFC Asset Classification and Provisioning 2026

Alongside this milestone, the RBI issued the Non-Banking Financial Companies Income Recognition, Asset Classification and Provisioning Directions, 2025, effective from 28 November 2025. This is the first time all IRACP rules for NBFCs have been consolidated into a single, standalone direction. It replaces every earlier prudential norm on income recognition and asset quality. If your NBFC is still applying pre-2025 provisioning norms or has not updated its internal classification systems to align with the new directions, you are in breach of the current regulatory framework.

This guide explains exactly what the new framework requires, how the four asset categories work, what provisioning rates apply, and what the RBI will examine during its next supervisory visit.

Important: 90-Day NPA Norm Is Now Final for All NBFCs from 31 March 2026

The NPA recognition glide path has completed. The timeline was as follows: accounts overdue more than 150 days were classified as NPA from 31 March 2024, accounts overdue more than 120 days were classified as NPA from 31 March 2025, and accounts overdue more than 90 days must be classified as NPA from 31 March 2026. This final stage applies to all NBFCs that were previously on the transition path. NBFCs already following the 90-day norm were not on the glide path and remain unaffected. For those completing the transition now, higher NPA numbers in March 2026 financial statements are expected. That is not a problem to hide. It is a compliance outcome to manage.

The IRACP Directions 2025: What Changed on 28 November 2025

Before the IRACP Directions 2025, NBFC provisioning rules were scattered across layer-specific master directions and several standalone circulars. The new directions consolidate everything into one document effective from 28 November 2025, and they introduce a more standardised, transparent framework that aligns NBFC accounting practices with international norms.

The directions apply to all NBFCs across Base, Middle, and Upper layers, with differentiated requirements as an NBFC grows in size and systemic importance. Income recognition rules are now explicitly objective, meaning income from a loan cannot be recognised simply because it falls within a repayment schedule. It must be based on actual repayment performance. On any account classified as NPA, income can only be recognised when it is actually received in cash. Accrual-based income recognition on NPA accounts is prohibited without exception.

Another significant clarification is the borrower-wise NPA rule. If any one credit facility of a borrower is classified as NPA, all other credit facilities extended to that same borrower by the same NBFC must also be classified as NPA. An NBFC cannot treat one loan as standard while another loan to the same borrower is in default. This rule prevents the practice of masking borrower-level stress by keeping some facilities performing on paper.

Special Mention Accounts: Catching Stress Before It Becomes NPA

The SMA framework exists to give both the NBFC and the regulator an early warning signal before a loan crosses into the NPA territory. SMA classification is based on the number of days a principal or interest payment is overdue at the day-end position. This is a technical but critical detail. Classification is not based on the position at month end or at the date of a management review meeting. It is based on the system's day-end snapshot.

| SMA Category | Days Overdue at Day-End | Required Action |

|---|---|---|

| SMA-0 | 1 to 30 days | Flag for enhanced monitoring, review borrower profile |

| SMA-1 | 31 to 60 days | Initiate borrower contact, review security, escalate internally |

| SMA-2 | 61 to 90 days | Mandatory reporting to CRILC for exposures above Rs. 5 crore |

| NPA | More than 90 days from 31 March 2026 | Stop income accrual, apply NPA provisioning norms immediately |

SMA-2 reporting to the Central Repository of Information on Large Credits is mandatory for all exposures of Rs. 5 crore and above. This means your credit monitoring system must be capable of generating SMA classifications at day-end and flagging borrowers for CRILC reporting automatically. An NBFC that relies on manual reviews to identify SMA accounts will almost certainly report late and trigger regulatory concerns about the quality of its early warning systems.

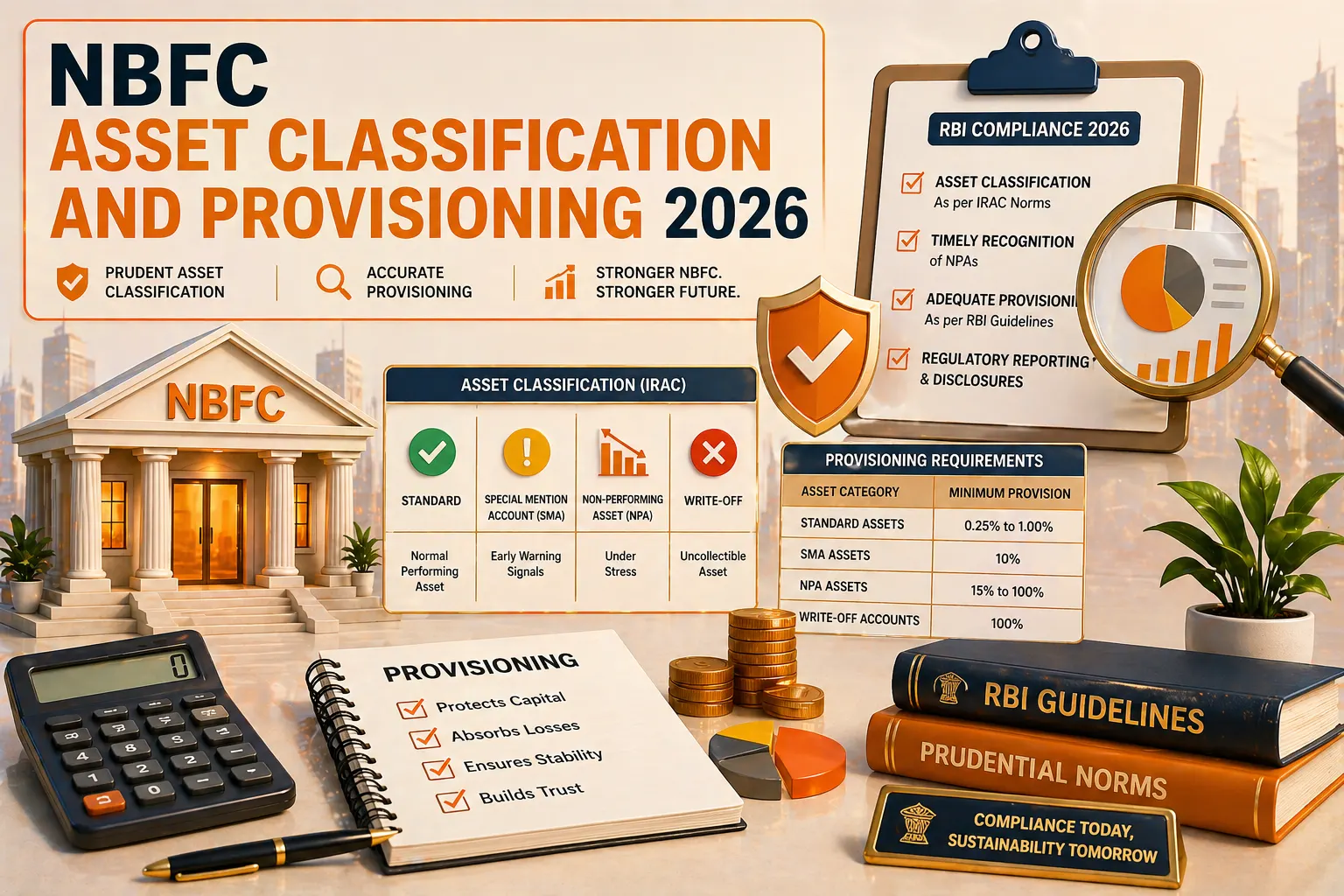

Four Asset Categories: Definitions You Must Apply Correctly in 2026

Every loan and credit exposure on an NBFC's books must be placed into one of four asset categories. The category determines how much provision must be held and whether income can be recognised. Getting the classification wrong, whether by classifying an NPA as standard or by not moving a sub-standard asset to doubtful on time, is a financial misstatement and a regulatory violation.

Standard Assets

A standard asset is one where repayment is proceeding as per schedule and there is no reason to doubt the borrower's ability to repay. Standard assets still attract provisioning requirements. For Base Layer NBFCs, the standard asset provision rate is 0.25 percent of outstanding loans. For Middle Layer and Upper Layer NBFCs, the rate is 0.40 percent. Infrastructure loans and commercial real estate exposures carry different standard asset provisioning rates. These provisions exist to build a buffer before stress becomes visible, not after.

Sub-Standard Assets

A sub-standard asset is any loan that has been NPA for a period not exceeding 18 months. When a restructured loan is renegotiated or rescheduled, it is also treated as sub-standard until it demonstrates 12 months of satisfactory repayment under the revised terms. The provisioning requirement for sub-standard assets is a general provision of 10 percent of the total outstanding amount. For the unsecured portion of a sub-standard asset, an additional provision of 10 percent applies, bringing the total to 20 percent for the unsecured component.

Doubtful Assets

A doubtful asset is one that has remained in the sub-standard category for more than 18 months. At this stage, the asset carries all the weaknesses of a sub-standard asset plus the additional uncertainty that full recovery is highly questionable because of deteriorating collateral value or other factors. Provisioning for doubtful assets varies based on how long the asset has been in the doubtful category. For the first year in doubtful status, the provision is 25 percent of the secured portion. This rises to 40 percent in the second year and 100 percent from the third year onward. The unsecured portion of any doubtful asset must be provisioned at 100 percent from the moment of classification.

Loss Assets

A loss asset is one that has been identified by internal or external auditors, or by an RBI inspection, as uncollectible or of such negligible value that its continuation as a productive asset is not justified. The entire outstanding amount of a loss asset must be provided for at 100 percent. Loss assets that are not written off immediately must still be fully provisioned. Keeping a loss asset on the books without 100 percent provisioning in the hope of a future recovery is not a permitted approach under the IRACP Directions 2025.

Provisioning Rates at a Glance: 2026 Framework

| Asset Category | Secured Portion Provision | Unsecured Portion Provision | Notes |

|---|---|---|---|

| Standard (Base Layer) | 0.25% of outstanding | 0.25% of outstanding | Higher for infra and CRE exposures |

| Standard (ML and UL) | 0.40% of outstanding | 0.40% of outstanding | Cannot be netted against gross NPA |

| Sub-Standard | 10% of outstanding | 20% of outstanding total | 10% general plus 10% for unsecured portion |

| Doubtful: Up to 1 year | 25% of secured portion | 100% of unsecured portion | From date of doubtful classification |

| Doubtful: 1 to 3 years | 40% of secured portion | 100% of unsecured portion | Security value assessed at realisable value |

| Doubtful: More than 3 years | 100% of secured portion | 100% of unsecured portion | Full provision regardless of security |

| Loss Assets | 100% of total outstanding | 100% of total outstanding | Write-off or full provision immediately |

NPA Upgradation: Only When All Overdues Are Cleared

One of the most significant discipline changes introduced by the RBI in recent years is the rule on NPA upgradation. An account that has been classified as NPA can only be upgraded back to standard status when all outstanding arrears of both principal and interest have been paid in full by the borrower. Partial payment of arrears, even if it brings the current overdue below 90 days, is not sufficient for upgradation.

This rule exists because partial payments were previously used to game the classification system. A borrower in genuine stress would make a minimal payment to keep the account just below the NPA threshold, deferring recognition of the true underlying problem. The current rule eliminates that approach. Until every rupee of overdue interest and principal is settled, the account stays classified as NPA and continues to attract NPA provisioning requirements.

The same principle applies to restructured accounts. An account that was restructured and moved to sub-standard classification must demonstrate 12 consecutive months of satisfactory repayment under the revised terms before it can be considered for upgradation. No shortcut exists within the IRACP Directions 2025.

Conclusion

NBFC asset classification and provisioning in 2026 is governed by a framework that is now fully consolidated, fully effective, and fully enforced. The IRACP Directions 2025 close every gap that existed in the previous system. The 90-day NPA norm has completed its glide path. The borrower-wise NPA rule prevents selective recognition of stress. The NPA upgradation rule prevents gaming through partial payments. And the provisioning rates for sub-standard, doubtful, and loss assets are now clearly prescribed with no ambiguity.

For NBFC promoters and compliance teams, the immediate priority is to ensure that internal loan management systems can classify assets at day-end automatically, generate SMA reports for CRILC submission, and compute provisions in line with the IRACP Directions 2025. Manual processes and spreadsheet-based tracking are no longer adequate for this level of precision. The RBI's supervisory teams know exactly what they are looking for and the discrepancies between policy and practice are getting harder to conceal.

Immediate Action Required for Your NBFC

Review your loan management system to confirm it classifies assets at day-end and applies the 90-day NPA norm without exception from 31 March 2026. Update your provisioning matrix to match the rates prescribed in the IRACP Directions 2025. Ensure CRILC reporting for SMA-2 accounts is automated for all exposures above Rs. 5 crore. Verify that your NPA upgradation process requires full clearance of all overdues before reclassification. An IRACP compliance review by a qualified NBFC specialist before your next statutory audit is strongly recommended.

Blog Summary

The RBI's NBFC Income Recognition, Asset Classification and Provisioning Directions, 2025, effective from 28 November 2025, consolidate all IRACP rules into a single framework for the first time. From 31 March 2026, the 90-day NPA norm applies to every NBFC in India, completing the glide path that began in 2022. The directions prescribe four asset categories: standard, sub-standard, doubtful, and loss, with provisioning rates ranging from 0.25 percent for standard assets in Base Layer NBFCs to 100 percent for loss assets. Sub-standard assets attract 10 percent general provision with an additional 10 percent for the unsecured portion. Doubtful assets attract provisions of 25 percent, 40 percent, and 100 percent on the secured portion depending on duration. Borrower-wise NPA classification means all facilities to a defaulting borrower must be classified as NPA simultaneously. NPA upgradation requires full clearance of all principal and interest overdues. SMA classification must be based on day-end positions, and CRILC reporting of SMA-2 accounts is mandatory for exposures of Rs. 5 crore and above.

Frequently Asked Questions

Q1. What is the borrower-wise NPA classification rule under the IRACP Directions 2025 and why does it matter?

The borrower-wise NPA classification rule requires that if any single credit facility extended to a borrower by an NBFC is classified as NPA, all other credit facilities provided by the same NBFC to the same borrower must also be classified as NPA simultaneously. This means an NBFC cannot maintain one loan to a borrower as a standard asset while another loan to the same borrower is already overdue beyond 90 days. The rule was introduced to prevent selective reporting of stress, where an NBFC would classify only the most visibly overdue facility as NPA while keeping related exposures as standard to suppress the true extent of borrower-level credit risk. Under the IRACP Directions 2025, the moment any one facility of a borrower crosses the NPA threshold, the NBFC must reclassify all other facilities to that borrower and apply the appropriate NPA provisioning norms across the entire exposure to that borrower. This has a significant impact on NBFCs that extend multiple products to the same borrower, such as a term loan alongside a working capital facility.

Q2. What are the provisioning requirements for doubtful assets in 2026 and how is the secured versus unsecured portion determined?

Doubtful assets are loans that have remained in the sub-standard category for more than 18 months. The provisioning rate for doubtful assets increases the longer the account remains in that category. During the first year in doubtful status, the NBFC must provision 25 percent of the secured portion and 100 percent of the unsecured portion. In the second and third year, the provision on the secured portion increases to 40 percent, while the unsecured portion continues to attract 100 percent provisioning. After three years in the doubtful category, the entire outstanding amount, both secured and unsecured, must be provisioned at 100 percent. The secured portion is determined based on the realisable value of the security to which the NBFC has valid legal recourse. This is not the original value of the security at the time of disbursement. It is the value at which the security could actually be sold in the current market. If the realisable value of the security has deteriorated significantly since disbursement, the portion treated as secured will shrink accordingly, which increases the effective provisioning requirement.

Q3. Under what conditions can an NPA account be upgraded back to standard status?

An account classified as NPA can only be upgraded to standard status when the borrower has paid all outstanding arrears of both principal and interest in full. There is no partial payment option. Bringing the current overdue below 90 days through a partial payment while leaving earlier arrears outstanding does not qualify the account for upgradation under the IRACP Directions 2025. For restructured accounts that were classified as sub-standard following a renegotiation or rescheduling, the condition for upgradation is different. These accounts must first demonstrate a minimum of 12 consecutive months of satisfactory repayment under the revised terms before they can be considered for reclassification to standard. The clock for this 12-month period starts only after the restructuring terms have been formally implemented. An NBFC that upgrades an NPA account before these conditions are fully met is making a classification error that will be identified during an RBI inspection or statutory audit, and will require provision reversal corrections in the financial statements.